New Zealand’s iGaming Market: On The Cusp Of Reform

New Zealand runs one of the few setups where a state betting monopoly coexists with unregulated online casino demand. And currently, according to Blask, offshore operators account for over 83 percent of iGaming demand in the country.

But change is coming. And fast.

New Zealand is on the cusp of legalising online casinos under a structure with no close parallels, making it one of the most compelling markets to watch right now.

Join iGamingFuture and Blask as we dive into New Zealand’s iGaming market on the eve of reform, unpacking the real size of the market and which brands are leading.

Blask metrics

Blask Index: A real-time measure of market demand volume for iGaming brands in a given country, based on normalised search data.

CEB (Competitive Earning Baseline): Projected revenue a brand should realistically capture given its market presence, expressed in USD as a min/avg/max range. A country’s CEB is the sum of the CEB of all brands present in a particular market.

Read more about Blask and its metrics: https://blask.com/blog/how-blask-measures/

The Regulatory Shift: A New Model

New Zealand is preparing to legalise online casinos, which are currently unregulated. Online sports betting is the exclusive dominion of TAB NZ – a state-run operator whose platform and operations are run by Entain under a long-term profit-sharing deal.

The Online Casino Gambling Bill, which has passed its third and final reading, now awaits Royal Assent and will cap the casino market at 15 licences, one per brand, with no operator permitted to hold more than three.

The licensing process is expected to begin in July 2026, with the broader rollout likely in the first half of 2027.

From December 2026, operators that have not applied must stop serving New Zealand residents. For most of them, obtaining a casino licence means operating without the sports betting vertical, as the law explicitly reserves that market to TAB NZ, handing Entain a powerful cross-selling advantage.

This model (state betting monopoly with an unregulated or prohibited casino vertical) is a relatively rare combination and can be found only in a handful of countries. According to Blask, New Zealand is the third largest of such markets after Turkey and South Korea.

The Market Right Now

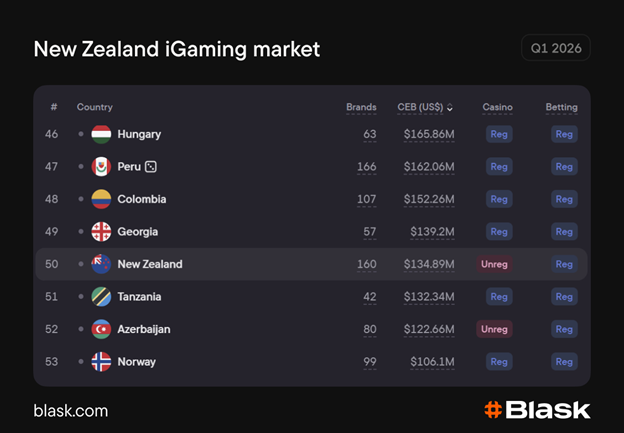

On a global scale, New Zealand is a middle-tier market. Blask ranks it 50th out of 126 by projected revenue (CEB). In Q1 2026, New Zealand’s CEB, according to Blask, was US$134.9 million (£99.7m), placing the country between Georgia and Tanzania.

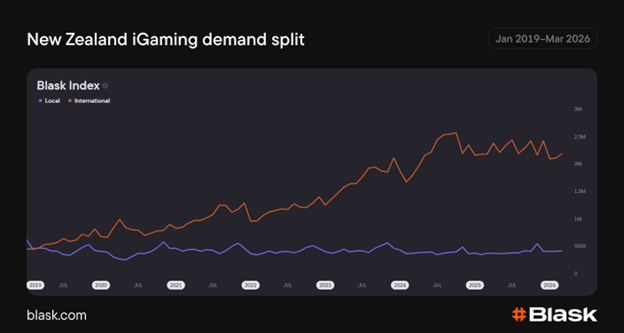

TAB NZ and its sub-brand Betcha account for only 14 percent of the total market CEB. In terms of user demand share, measured by the Blask Index, their performance is slightly stronger. As of March 2026, local operators accounted for 16.9 percent of the country’s Blask Index.

Back in early 2019, the local share of the Blask Index was over 57 percent. Total demand has grown almost 2.5x since then. Demand for international brands grew 3.7x, but for local brands it fell 10.7 percent.

Currently, 160 iGaming brands are competing for user attention in New Zealand.

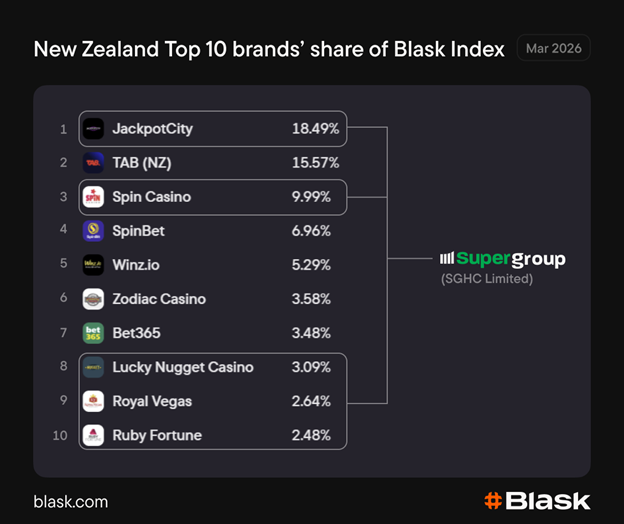

Offshore casino operator JackpotCity is the market leader, almost 3 percentage points ahead of TAB NZ. It is one of the oldest brands in the market, belonging to Super Group (SGHC Limited) – an international company that owns Betway.

Remarkably, SGHC Limited owns four more brands from the current top 10 in New Zealand (Spin Casino, Lucky Nugget Casino, Royal Vegas and Ruby Fortune).

In total, Super Group’s brands from the top 10 account for almost 37 percent of the country’s Blask Index. All top 10 brands are responsible for approximately 68 percent of total demand.

Who Will Benefit From The New Regime

New Zealand’s proposed model has no direct analogue. The closest comparisons are Slovenia and Switzerland. Both combine a state betting monopoly with licensed online casino operations, but tie casino licences to existing land-based operators. New Zealand has five land-based casinos, but licences are open to any operator that meets the criteria.

For most operators currently in the market, the new framework is a casino-only opportunity (with sports betting locked in place at TAB NZ). Entain is the exception. It already runs TAB NZ’s operations under a 25-year partnership and has publicly said it is vying for three of the new casino licences.

«We are confident that we’ll probably get three of those licences. And I think the opportunity for us is significant because we’ll be the only player who will be able to do cross-sell».

Stella David, CEO of Entain

5 March 2026, the company’s FY25 results presentation

Bottom Line

New Zealand chose an unusual path to legalise online casino. The rationale is channelisation: Shifting existing demand into a regulated system. But how much of it moves will depend on the enforcement.

Of the 15 licences, Entain has publicly committed to bidding for three. Super Group, which already holds five of the top ten brands by Blask Index, would face the same three-licence cap if it applies, leaving just nine licences up for grabs for the rest of the market.