Denmark’s Gambling Reforms: Early Signs Of Offshore Migration?

Denmark has long been one of Europe’s top regulated gambling jurisdictions, with high channelisation and a large licensed sector. But recent reform proposals have triggered concerns that tighter restrictions could push part of player activity toward offshore brands.

Blask data shows a short-lived increase in offshore interest after the announcements.

But the effect faded quickly, with the overall traffic distribution changing very little.

Since most restrictions have not entered into force, the current data reflects reaction to the reform news rather than the long-term impact of the measures themselves.

Blask metrics

BAP (Brand’s Accumulated Power): A brand’s share of total market demand in a given country and period

CEB (Competitive Earning Baseline): Projected revenue a brand should realistically capture given its market presence, expressed in USD. A country’s/province’s CEB is the sum of CEB of all brands present in a particular market.

Context Behind New Regulation

For years, Denmark has been viewed as one of Europe’s most stable regulated gambling systems. A high channelisation rate and relatively open licensing model have kept most player activity inside the legal sector instead of pushing them toward offshore operators.

But that reputation came under pressure after the government introduced a new reform package known as Spilpakken 1, although most of the restrictions are scheduled to take effect later in 2026.

The measures include a whistle-to-whistle ban on betting advertising during live sports broadcasts, tighter restrictions on outdoor gambling promotions and new limits around free-to-play bonuses and marketing activity.

The announcement has triggered concerns across the industry that stricter advertising rules could gradually shift part of the audience toward offshore brands.

Some operators and analysts have also warned that the new approach could weaken the balance that previously made the country one of the leading examples of pragmatic gambling regulation in Europe.

But the key and most compelling question now is whether players have already started reacting to the upcoming restrictions, even before most of the measures officially enter into force.

How The Market Reacted

The reform announcement immediately raised one question: Would Danish players shift toward offshore operators?

Early market reaction suggests some increase in interest outside the regulated sector, although the overall balance saw very little change.

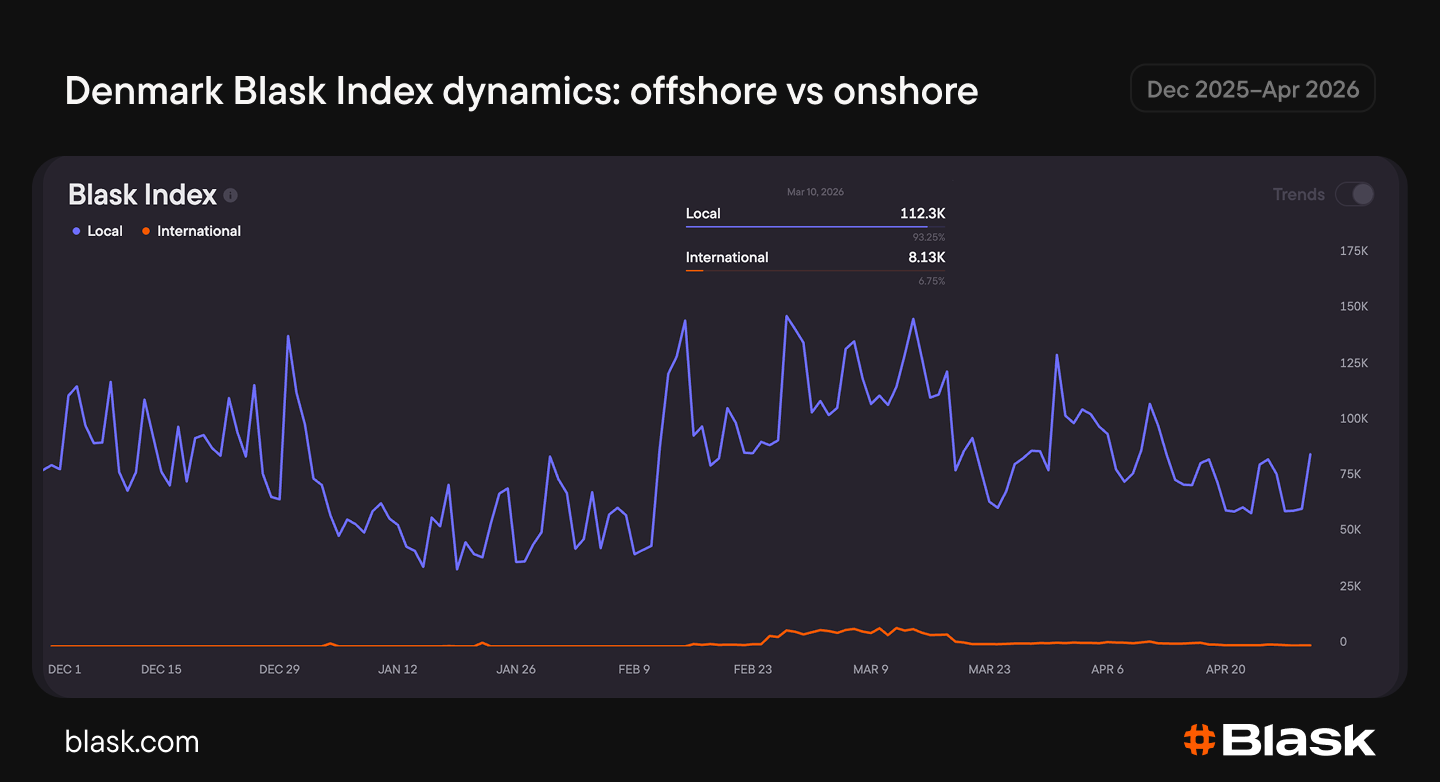

Offshore Interest Increased Following The Reform Announcement

The daily Blask Index data between December 2025 and May 2026 shows a largely unchanged distribution throughout the period.

Licensed local operators consistently dominated Danish demand, while offshore brands accounted for only a small share of tracked activity.

The only visible deviation came between late February and mid-March, shortly after the reform package was announced.

Offshore traffic temporarily climbed to roughly six-to-seven percent of total tracked activity, but the increase proved short-lived and the previous balance returned within a few weeks.

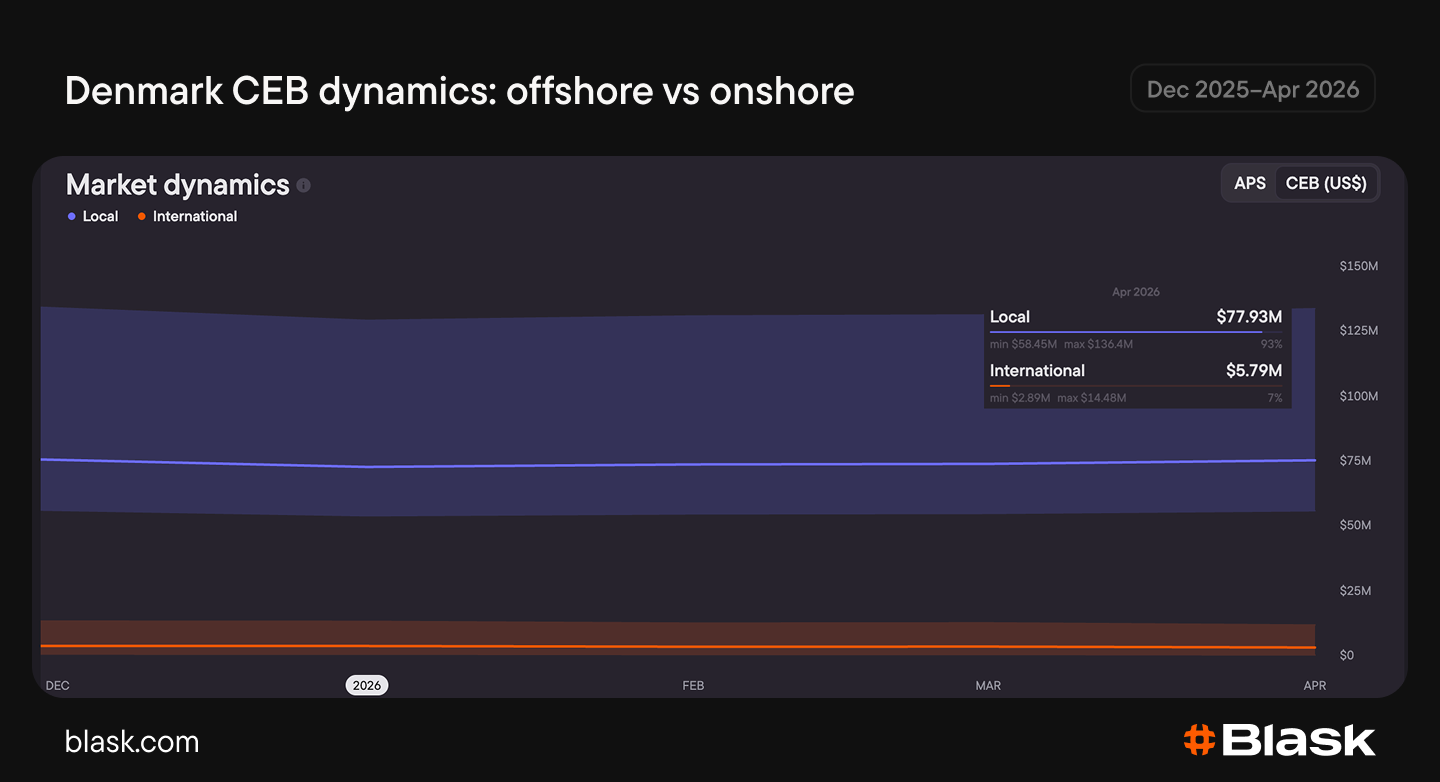

CEB Distribution Largely Unchanged

Monthly CEB data between December 2025 and April 2026 points to a similar pattern.

Offshore operators consistently accounted for roughly seven-to-eight percent of total projected revenue while licensed local brands controlled more than 90 percent throughout the period.

Even during the March spike, the broader distribution barely moved. Interest in offshore brands increased after the reform announcement, but the shift proved limited and temporary rather than structural.

So far, the data only partially confirms concerns about a migration toward offshore platforms.

Overall, while the reform news triggered a short-term increase in offshore interest, the spike disappeared within weeks and did not materially reshape the market.

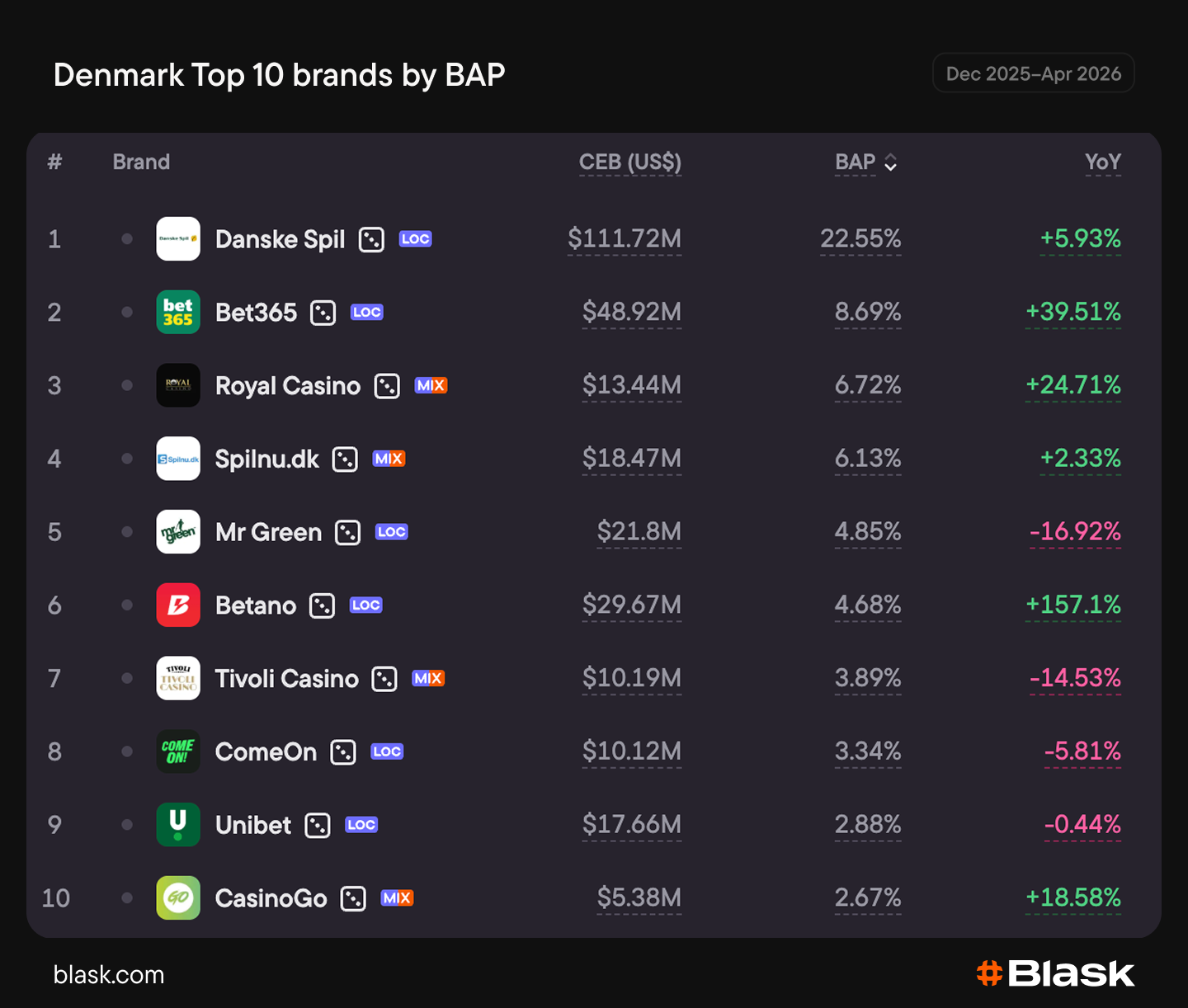

Brand-Level Situation Changed Very Little

Brand rankings show limited movement after the reform announcement.

Only one operator in the top 30 BAP ranking operates without a Danish license: Rainbet.

Nearly the entire leaderboard still belongs to licensed operators, which supports Denmark’s high channelisation level.

State-owned brand Danske Spil kept a comfortable lead over competitors. In April 2026, the operator held just above 26 percent BAP, almost identical to December 2025.

While bet365 kept second place and gained some share, Royal Casino, Spilnu.dk, Mr Green, Betano and Tivoli Casino all stayed inside the leading tier.

The operator mix also looked relatively broad.

In April 2026, 21 brands held BAP shares above 1 percent, so traffic and attention were not concentrated around only a few operators.

The comparison between December and April shows only minor ranking shifts, as bet365 and Royal Casino improved their positions slightly, Spilnu.dk and Tivoli Casino lost some share, and Bet25 entered the top group by April.

The broader hierarchy stayed largely intact during the period.

Bottom Line

Early data does not show any major shift away from Denmark’s regulated gambling sector.

Interest in offshore operators increased briefly after the reform announcement but the spike faded quickly. Licensed brands still control the overwhelming majority of activity.

Brand rankings showed only minor changes between December 2025 and April 2026.

The biggest market changes will likely appear later, once the new restrictions officially enter into force and players respond to the rules in practice rather than to the announcement itself.