How Peru Got iGaming Regulation Right And Grew Demand By 120 Percent

Two years after Peru launched its regulated iGaming market in February 2024, the country has become one of LatAm’s clearest success stories.

Offshore brands have been largely pushed out, players have stayed with the platforms they already trusted and demand has continued to grow.

In this article, iGamingFuture and Blask examine what the data actually shows – and why Peru’s model worked.

This is a fascinating lesson in how regulatory frameworks can win the channelisation battle and beat the bad market.

Blask metrics overview

Blask Index: Real-time measure of market demand volume for iGaming brands in a given country, based on normalised search data.

BAP (Brand’s Accumulated Power): A product’s share of total demand in a particular country.

CEB (Competitive Earning Baseline): Projected revenue a brand should realistically capture given its market presence, expressed in USD.

How Peru Built Its Market

Before 2022, online gambling and betting in Peru had no legal framework. Operators worked in a grey area and players had no regulated options.

That changed with Law No. 31557, which created a regulatory structure from scratch and appointed MINCETUR, the Ministry of Foreign Trade and Tourism, as the regulator.

But the first version of the law had one significant gap: It didn’t allow international operators to obtain local licenses.

This altered in June 2023, when Law No. 31806 amended the original legislation and opened the door to global brands. In hindsight, this proved to be the decision that would shape the market.

February 9, 2024, marked the start of the full regulatory regime.

Before this, there was an amnesty period and operators that had already been active in the market were given until March 10 to submit licence applications without penalty.

After that, the window slammed shut. While the transition period was relatively short, it was enough to set the market’s direction.

How Peru’s Market Is Growing

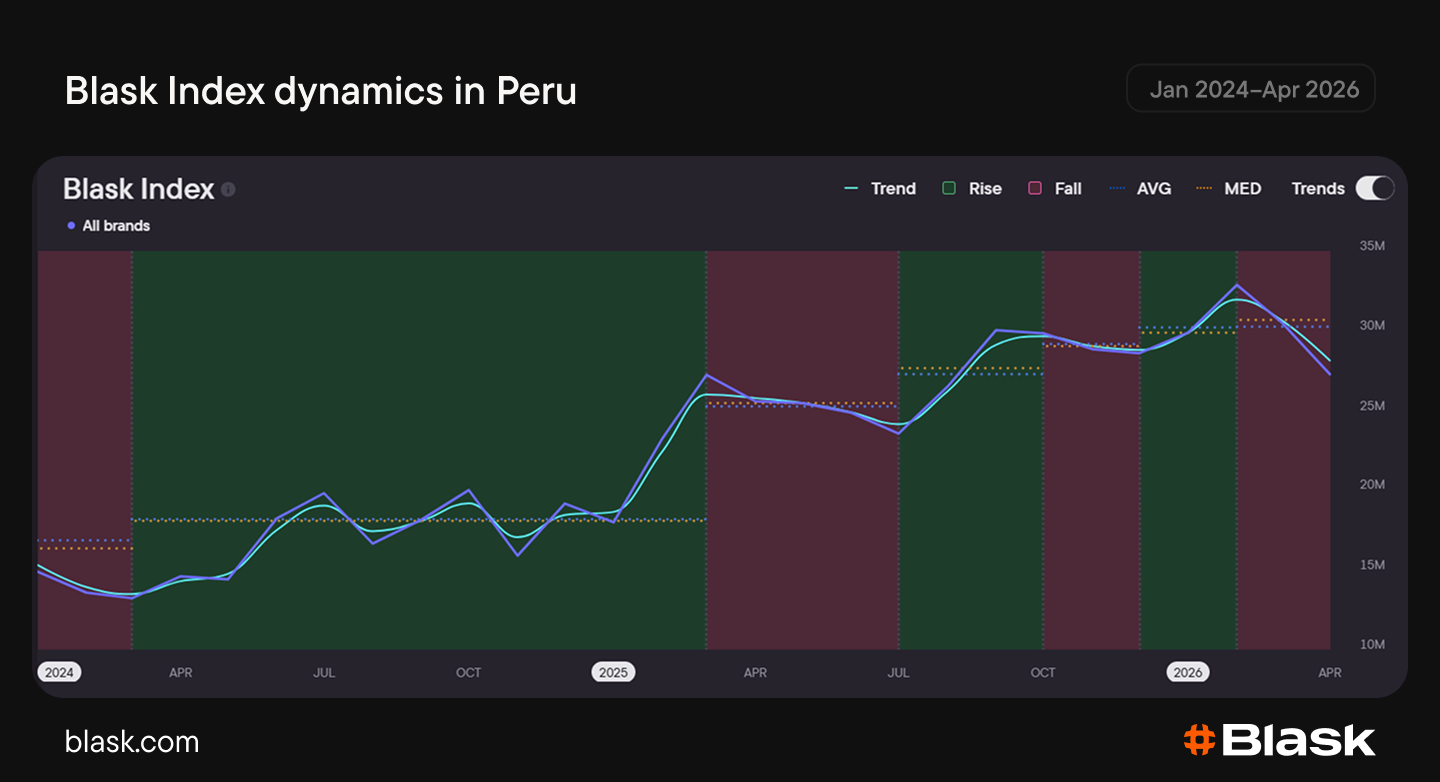

The launch of the full regulatory regime was accompanied by a brief dip in users’ demand – a typical pattern during market transitions, when both operators and players are adjusting to a new framework. But by summer 2024, the Blask Index was already trending upward again.

From January 2024 to April 2026, demand grew by 120 percent.

The trajectory has been consistently positive throughout the period, except for seasonal slowdowns in spring. This pattern appeared in both 2025 and 2026, suggesting a cyclical rather than structural dynamic.

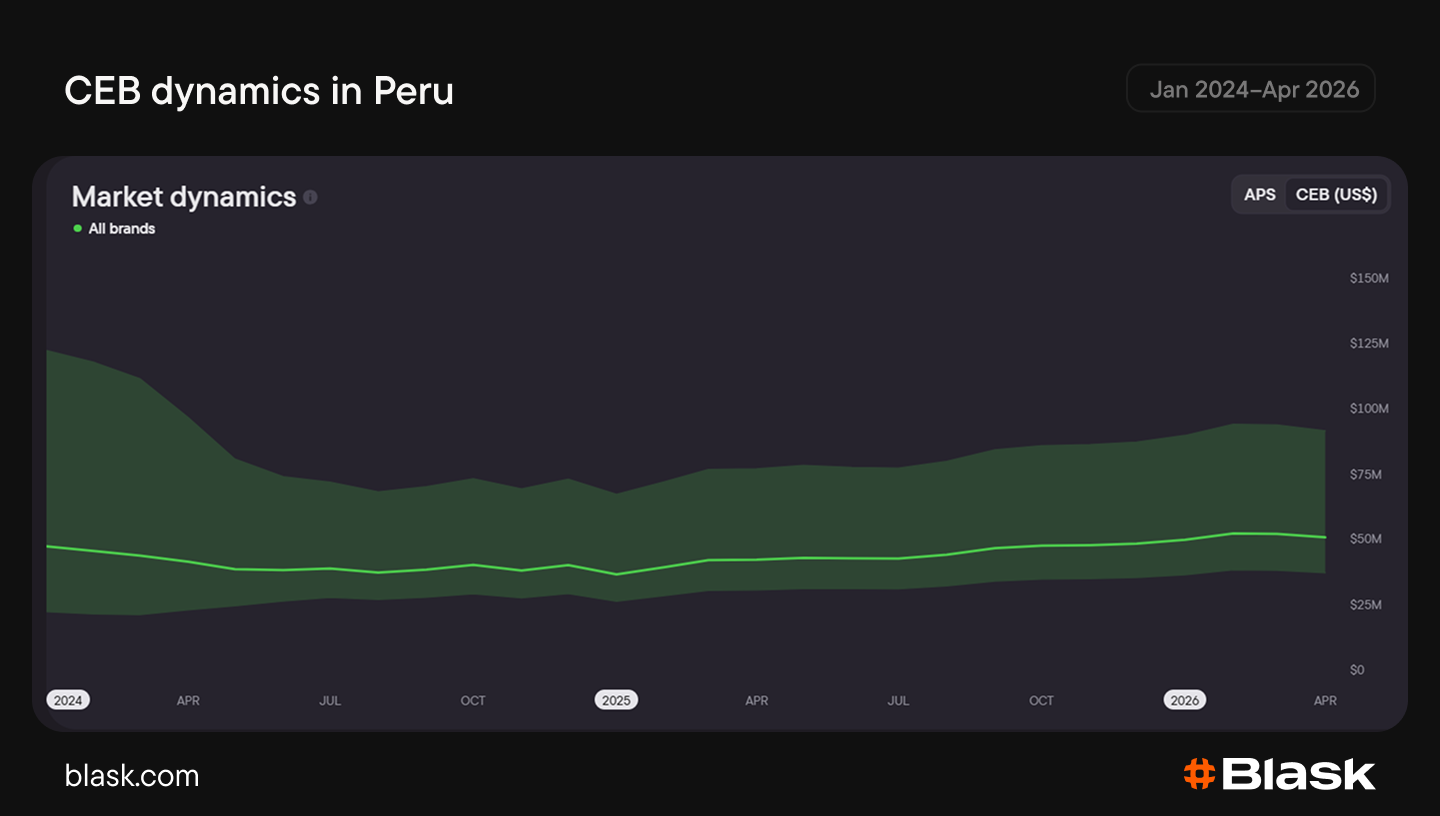

While demand has grown steadily, projected revenue has remained relatively flat over the same period, increasing just 10 percent since January 2024.

Interest is rising faster than actual spending, which is typical for a market still finding its footing. Monetisation hasn’t caught up yet, but the trajectory of demand suggests that it eventually will.

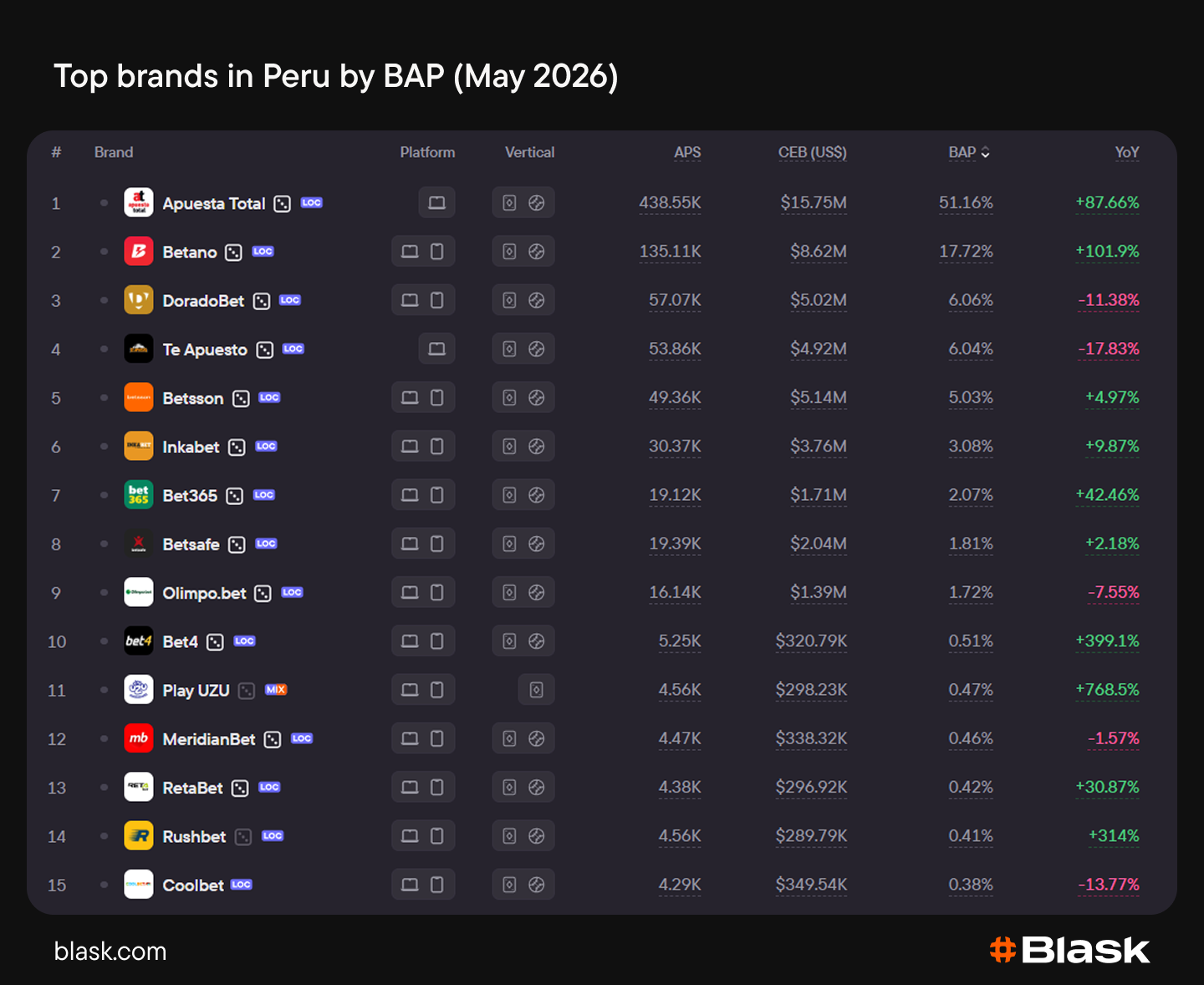

Biggest Brands: Apuesta Total Dominates, But Betano’s Closing The Gap

At the brand level, the Peruvian market has a clear leader: Apuesta Total holds 51.16 percent BAP, commanding more than half of total demand, and is, for now, in a league of its own.

Behind it, Betano has grown 101.9 percent year-over-year and now sits at 17.72 percent BAP – crossing the 10 percent threshold that it had not reached in 2025.

If Betano’s momentum holds, Peru could gradually shift from a one-brand market to a more competitive one.

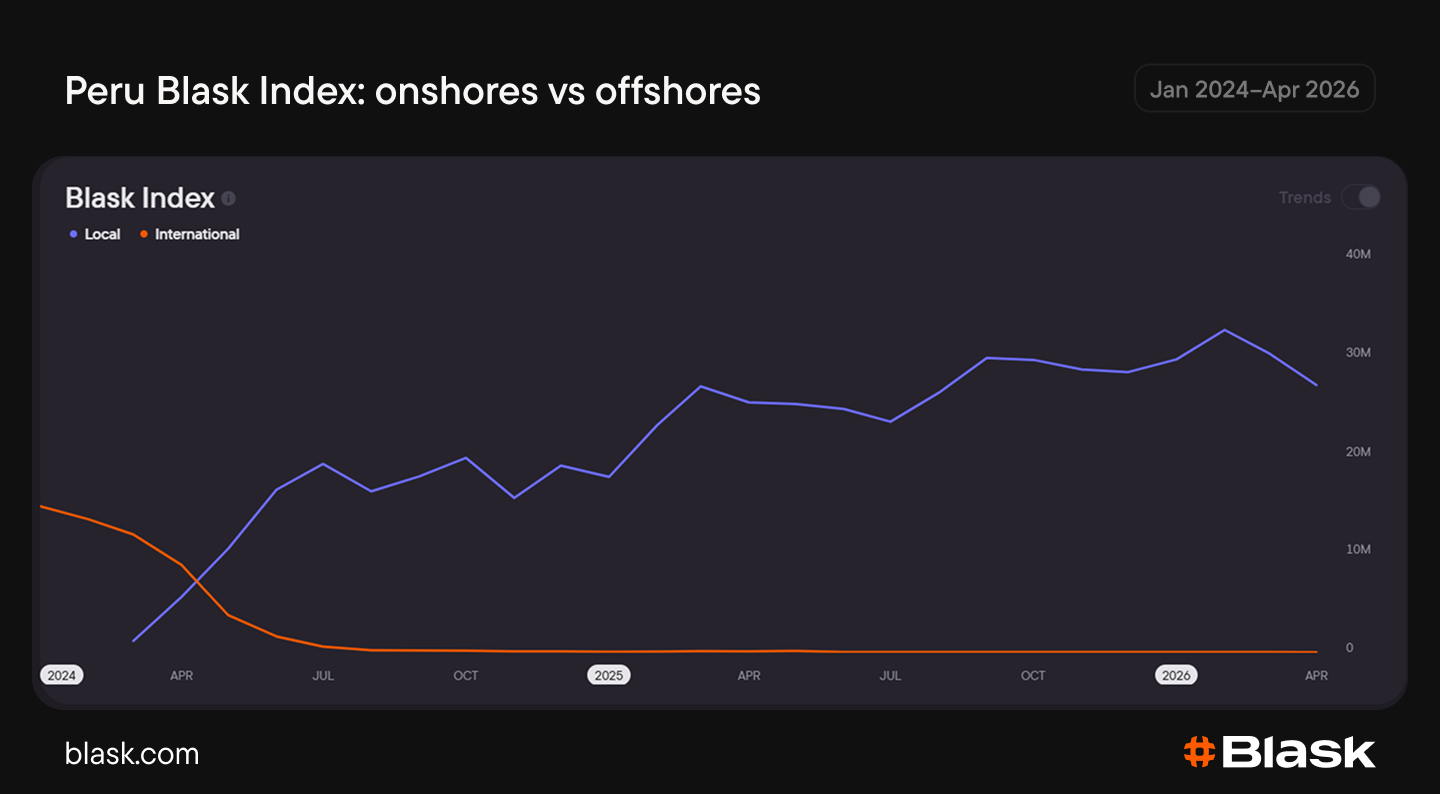

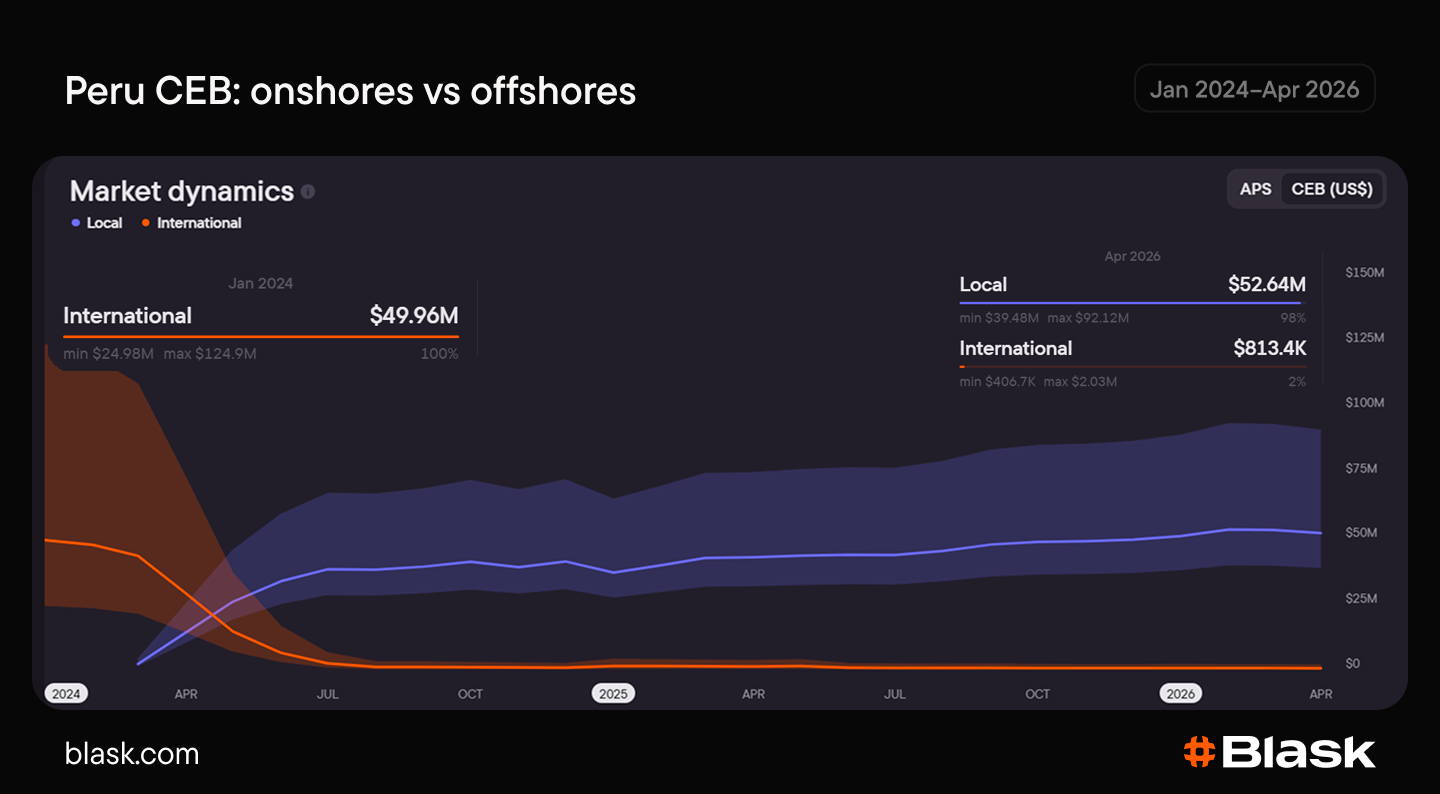

Onshore Vs Offshore: Who’s Winning

The shift happened quickly. When the regulatory window closed in March 2024, the Blask Index for offshore brands dropped sharply, while interest in licensed operators moved in the opposite direction.

Since July 2024, offshore visibility has remained below one percent and has not recovered.

Low visibility translates to low CEB: The offshore share of projected revenue has remained at two-to-four percent since mid-2024. Under current conditions, this balance is unlikely to shift.

International Brands: A Winning Strategy

Peru proves that players tend to stay with brands they already trust, but only when those brands localise.

For example, Betano, Bet365, DoradoBet, BetSafe, Betsson, Coolbet, and others all ranked within the top 15. And in 2026 they’re still in the top.

The contrast with other regulated markets makes this clearer.

Compare this with Rhode Island: Before iGaming legalisation (June 2023), the top leaderboard in this U.S. state was filled with specific brands. After legalisation, only one secured a domestic license; the rest became offshore operators. And now, nearly three- years-later, offshore brands still dominate because players never switched.

Peru’s regulatory model is also commercially attractive. While online casino operators in Brazil pay 12 percent tax on GGR, Peruvian operators pay the same rate but on NGR.

The Bottom Line

The data shows how regulation can absorb an existing offshore market into the licensed system, winning the channelisation battle by almost eliminating interest in offshore sites.

Peru also shows that allowing international brands to obtain local licences can help build a strong, regulated market, preserving competition without disrupting consumer choice.

Demand is currently growing faster than projected revenue, suggesting Peru still has room for further market maturation.

And while Apuesta Total currently dominates BAP, Betano’s rapid growth proves that there’s still everything to play for. The competitive landscape remains far from settled.