Finland is one of Europe’s last great gambling monopolies. But things are changing. With the competitive market set to open in July 2027, the state era is finally coming to an end – marking a major turning point.

In this article, iGamingFuture–in collaboration with Blask–explores early data that reveals how the market is already shifting.

End Of A Monopoly

For decades, all online gambling activity in Finland has been run by the state-owned Veikkaus Oy.

But in December 2025, the Finnish parliament approved a new iGaming bill, opening the path towards a competitive licensing model.

Operator licensing applications are now open, and the regulated, competitive market is expected to launch in July 2027.

Using Blask data, we captured the very first snapshot of how Finland’s competitive landscape is shifting – not after the new regime launches, but now, in the so-called “anticipation phase”.

This is a baseline, not a conclusion. Yet it already shows clear movement, with offshore brands collectively rising to challenge Veikkaus’ hitherto dominant market share.

Blask Metrics Explainer

Blask Index: Real-time measure of market demand volume for iGaming brands in a given country, based on normalised search data.

BAP (Brand’s Accumulated Power): A brand’s percentage share of total market demand in a specific country and period.

CEB (Competitive Earning Baseline): Projected revenue a brand should realistically capture given its market presence, expressed in USD.

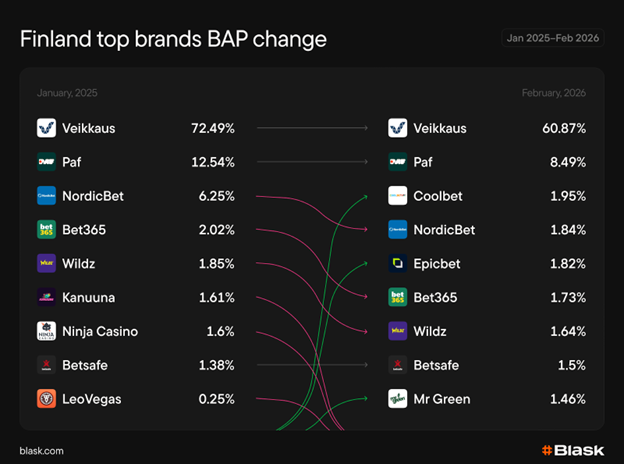

Brand Leaderboard, One Year Apart

The scale of the shift is visible: Out of an estimated US$645 million (£488.6m) in total CEB for 2025, offshore brands now account for roughly 50.5 percent, edging ahead of Veikkaus’ 49.5 percent.

Comparing brand rankings for January–February 2025, against the same period in 2026, Veikkaus remains the clear number one. But its BAP share dropped from 72.49 percent to 60.87 percent. That’s nearly 12 percentage points redistributed to other brands in a single year.

Where did that share go?

Partly to newcomers that weren’t on the radar at all in 2025, we discern.

Coolbet jumped straight to number three, Epicbet to number five and Mr Green entered in ninth place. None of these brands appeared in last year’s top list.

The brands that were already present mostly held their ground: Bet365 and Wildz each moved down a couple of positions and Betsafe nudged up from 1.38 percent to 1.50 percent.

NordicBet, however, saw a significant drop – from 6.25 percent to 1.84 percent, sliding from number three to number four.

The bigger losers are at either end of the table – Paf dropped from 12.54 percent to 8.49 percent. And three names from the 2025 top 10–Kanuuna, Ninja Casino and LeoVegas–were pushed out entirely by the new entrants.

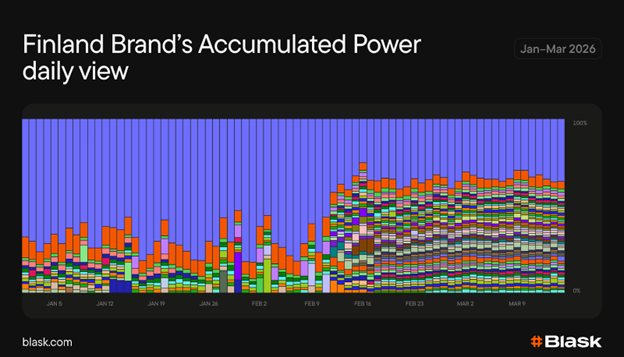

These shifts become even more telling when we zoom into the daily data, particularly around mid-February, when consumer search interest patterns changed noticeably.

The February Inflection Point

Looking at BAP dynamics in daily granularity across Q1 2026, the picture is stable through January and early February. Veikkaus dominates the chart as a solid block, with minimal challenger activity at the margins. Then, around mid-February, the composition visibly fractures.

New brands begin appearing in the daily BAP breakdown, and Veikkaus’ share compresses. This isn’t a gradual erosion. As the data reveals, the shift happened within days.

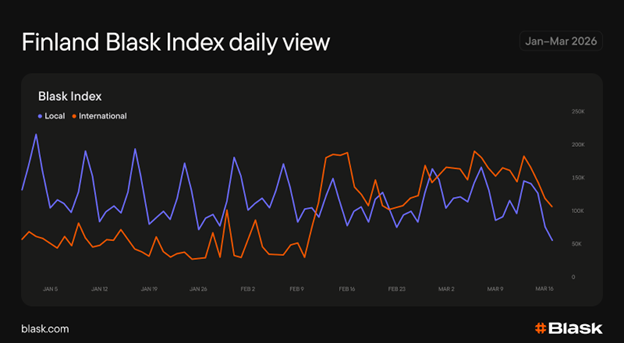

Blask Index, which tracks search interest for gambling brands split by local and international operators, confirms the same timing from the demand side.

Through January and into early February, local search activity held steady, while international search interest sat noticeably lower.

Then, around mid-February, offshore search activity surged, climbing to match–and at times exceed–onshore levels. Players were actively seeking out international alternatives – alongside, not instead of, Veikkaus.

Bottom Line

This is a starting point, not a finished picture.

Veikkaus still commands over 60 percent of market demand.

But the announcement alone has already shifted both brand activity and player behaviour.

And the competitive market is already taking share, before the regulatory framework is fully in place.