America’s illegal online gambling market is booming – and it’s far bigger than most realise. New research from AI market analysts Blask estimates that only about one-third of online gambling revenue in the U.S. is generated on regulated platforms, while some 70 percent flows offshore to sites beyond regulators’ reach.

For years, the black market has been notoriously difficult to measure. Offshore platforms, by nature, operate in the murky shadows of the underground economy, do not publish accounts and do not answer to regulators.

But now Blask has pulled back the curtain on this hidden world and is naming operators. Using AI to analyse user search patterns and estimate revenues based on visibility, influence and competition, the data reveals a rare view of the entire–not just regulated–U.S. market.

Big Business

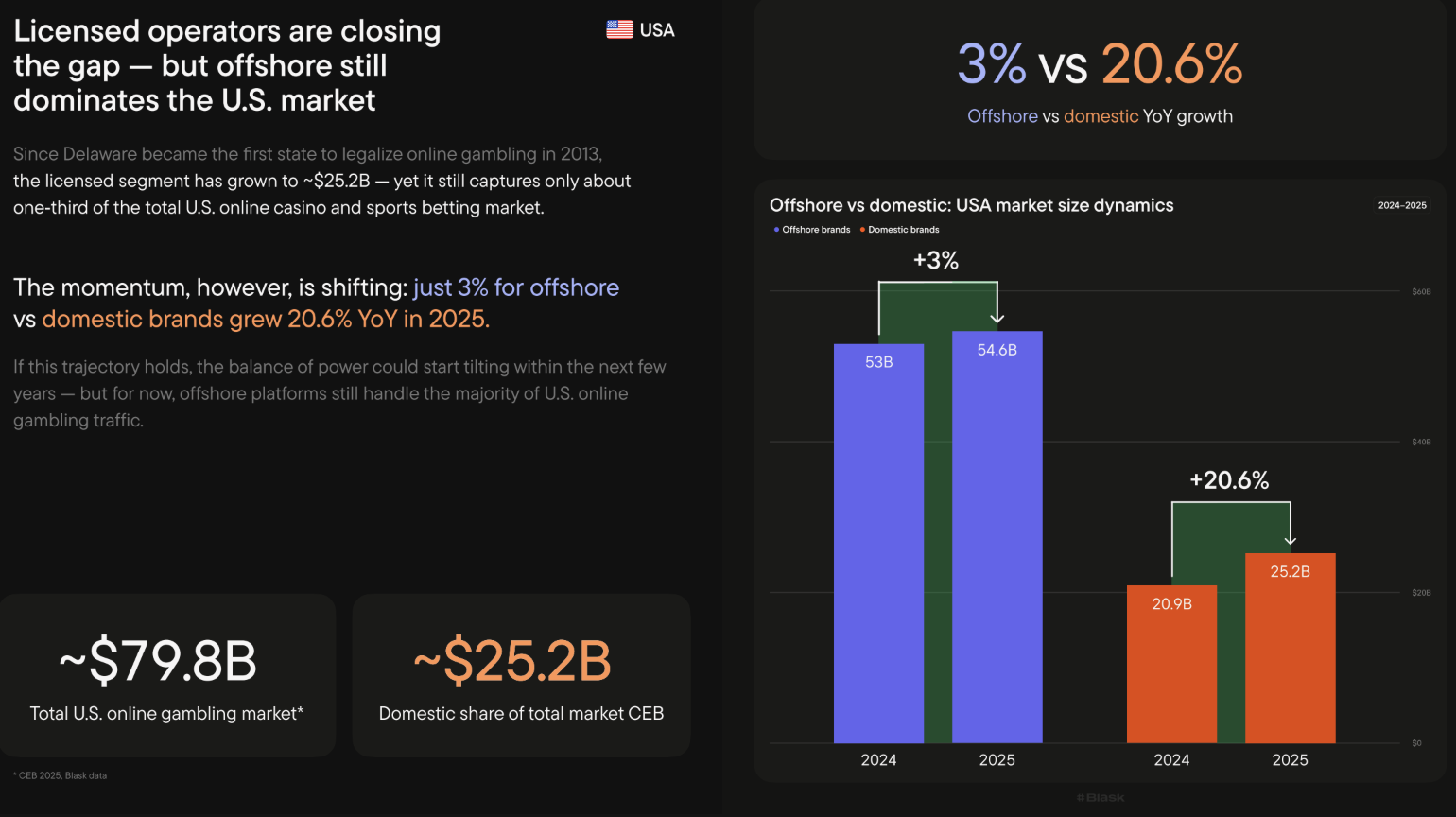

The data estimates the total U.S. online gambling market was worth US$79.8 billion (£60bn) in 2025, but only US$25.3 billion (£19bn) was generated by U.S. licensed operators – under one-third of the total market.

This figure is based on what Blask calls Competitive Earnings Baseline (CEB), an AI estimate of what a brand should earn based on its visibility and competition. It is not a financial forecast or official report, and it does not capture how many of those searches actually convert into players.

By using search engine query data, Blask also reveals the offshore operators offering services to U.S. players without onshore licensing.

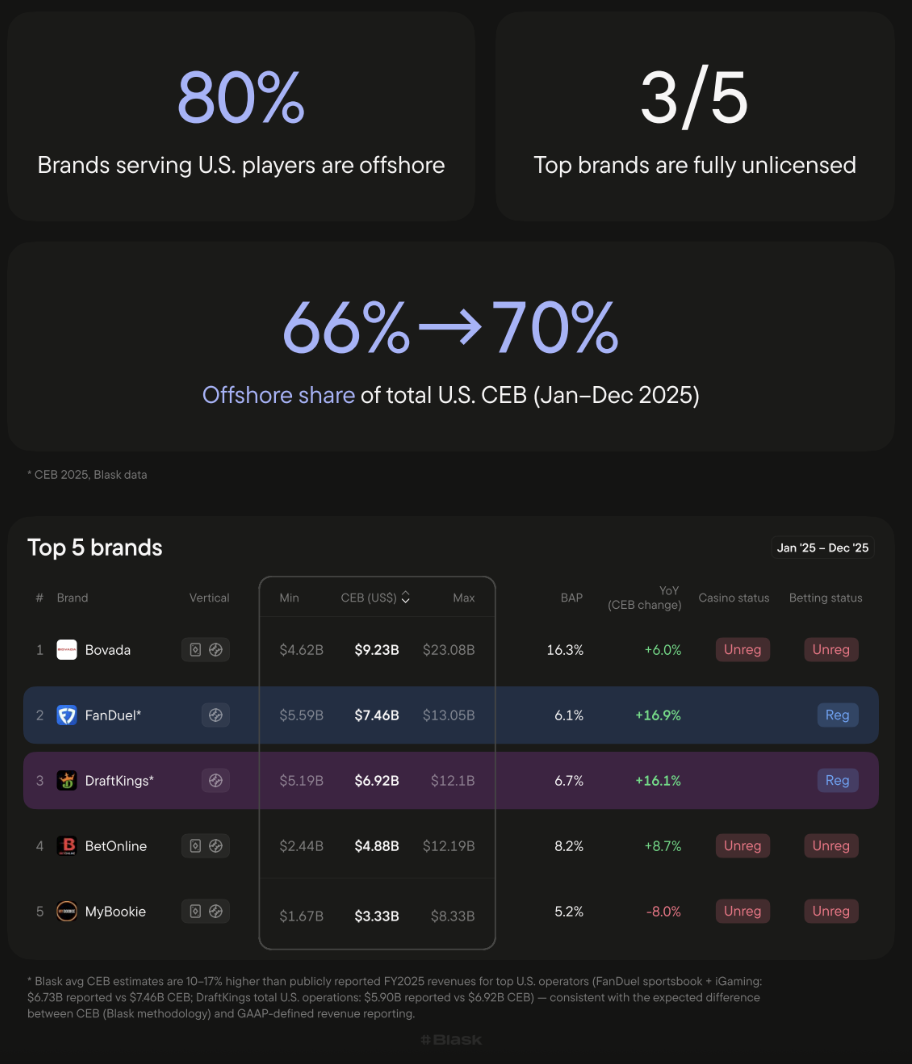

362 brands are active in the U.S., but only 72 are state-regulated – leaving around 80 percent, or 290 brands, operating outside local licensing requirements and consumer safeguards.

The good news: While the domestic market grew by 20.6 percent year on year, the offshore market only increased by 3 percent.

These figures build on and add colour to the scale of the issue as highlighted by other industry bodies, like the American Gaming Association (AGA).

As per the last AGA estimates, the illegal gambling industry was generating US$53.9 billion (£40.3bn) in revenue annually and costing state governments a potential of US$15.3 billion (£11.4bn) in lost taxes.

Bovada Leads

According to Blask, offshore operator Bovada–subject to cease-and-desist orders in a swathe of U.S. states, including Massachusetts, West Virginia, Tennessee, Pennsylvania, Kansas and Louisiana last year–was leading the market. Bovada operates under a licence from Curaçao eGaming.

In second place is the U.S.-regulated market leader, Flutter Entertainment’s FanDuel, followed by Massachusetts-origin DraftKings in third.

Two offshore operators, BetOnline and MyBookie, took fourth and fifth place.

Maturity Curve

The dominance of offshore gambling was not uniform across the U.S. – it depended heavily on what form of gambling was allowed.

In states where only sports betting is legal, offshore operators continue to thrive, accounting for around 74 percent of CEB.

But where both sports betting and online casino gaming are permitted, the balance begins to shift. The offshore share drops to 38 percent, with 62 percent of activity taking place on state-regulated platforms.

And it wasn’t just the types of gambling permitted that affected the revenue share. Market maturity also played a crucial role.

Blask found that newer markets still struggled to pull players away from offshore sites. States like Rhode Island, one of the most recent to roll out full iGaming, remained below the halfway mark.

But more established markets told a very different story.

In New Jersey, one of the earliest adopters of online gambling, regulated operators now capture around 73 percent of activity.

This led the report’s authors to conclude that: “Channelisation is a process, not a switch. Full-spectrum regulation works – but it takes time”.